Breaking news

World arms sales Top 100 arms companies grow despite supply chain challenge.

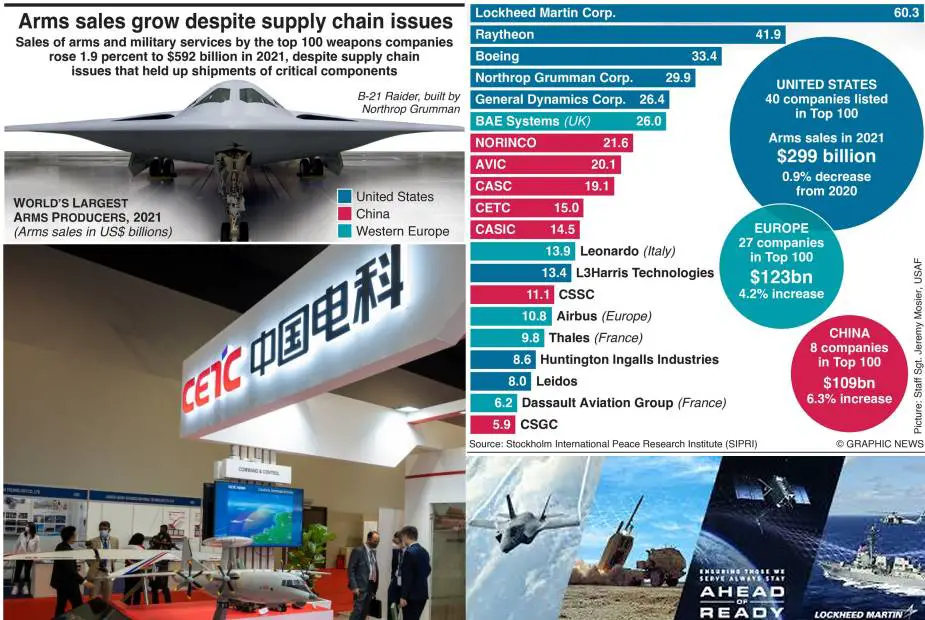

Sales of arms and military services by the 100 largest companies in the industry reached $592 billion in 2021, a 1.9 percent increase compared with 2020 in real terms. This is according to new data released on 5 December 2022 by the Stockholm International Peace Research Institute (SIPRI).

Follow Army Recognition on Google News at this link

Graphic Top 20 defense companies in the world. (Picture source Graphic News )

The increase marked the 7th consecutive year of rising global arms sales. However, while the rate of growth in 2020–21 was higher than in 2019–20 (1.1 percent), it was still below the average for the four years leading up to the Covid-19 pandemic (3.7 percent).

Supply chain issues seen in 2021 likely to worsen due to the Ukraine war

Many parts of the arms industry were still affected by pandemic-related disruptions in global supply chains in 2021, which included delays in global shipping and shortages of vital components.

‘We might have expected even greater growth in arms sales in 2021 without persistent supply chain issues,’ said Dr Lucie Béraud-Sudreau, Director of the SIPRI Military Expenditure and Arms Production Programme. ‘Both larger and smaller arms companies said that their sales had been affected during the year. Some companies, such as Airbus and General Dynamics, also reported labour shortages.’

Russia’s invasion of Ukraine in February 2022 has added to supply chain challenges for arms companies, not least because Russia is a major supplier of raw materials used in arms production. This could hamper ongoing efforts in the United States and Europe to strengthen their armed forces and to replenish their stockpiles after sending billions of dollars worth of ammunition and other equipment to Ukraine.

‘Increasing output takes time,’ said Dr Diego Lopes da Silva, SIPRI Senior Researcher. ‘If supply chain disruptions continue, it may take several years for some of the main arms producers to meet the new demand created by the Ukraine war.’

While reports indicate that Russian companies are increasing production because of the war, they have had difficulty accessing semiconductors. They are also being impacted by war-related sanctions. For example, Almaz-Antey (not included in the Top 100 for 2021 due to lack of data) has stated that it has not been able to receive payments for some of its arms export deliveries.

US companies dominate the Top 100, but sales decline

The arms sales of the 40 US companies in the listing totalled $299 billion in 2021. North America was the only region to see a drop in arms sales compared with 2020. The 0.8 per cent real-term decline was partly due to high inflation in the US economy during 2021. Since 2018, the top five companies in the Top 100 have all been based in the USA.

A recent wave of mergers and acquisitions in the US arms industry continued in 2021. One of the most significant acquisitions was Peraton’s purchase of Perspecta, a government IT specialist, for $7.1 billion.

‘We can probably expect to see stronger action from the US government to limit arms industry mergers and acquisitions in the next few years,’ said Dr Nan Tian, SIPRI Senior Researcher. ‘The US Department of Defense has expressed concern that reduced competition in the industry could have knock-on effects on procurement costs and product innovation.’

Europe: Aerospace sales fall, shipbuilding rises

In 2021 there were 27 Top 100 companies headquartered in Europe. Their combined arms sales increased by 4.2 per cent compared with 2020, reaching $123 billion.

‘Most of the European companies that specialize in military aerospace reported losses for 2021, which they blamed on supply chain disruptions,’ said Lorenzo Scarazzato, a researcher with the SIPRI Military Expenditure and Arms Production Programme. ‘In contrast, European shipbuilders seem to have been less affected by the pandemic fallout and were able to increase their sales in 2021.’

Dassault Aviation Group bucked the trend in the military aerospace sector. The company’s arms sales saw a sharp 59 per cent increase to $6.3 billion in 2021, driven by deliveries of a total of 25 Rafale combat aircraft.

Chinese companies drive rapid growth in Asian arms sales

The combined arms sales of the 21 companies in Asia and Oceania included in the Top 100 reached $136 billion in 2021—5.8 per cent more than in 2020. The eight Chinese arms companies in the listing had total arms sales of $109 billion, a 6.3 per cent increase.

‘There has been a wave of consolidation in the Chinese arms industry since the mid-2010s,’ said Xiao Liang, a researcher with the SIPRI Military Expenditure and Arms Production Programme. ‘In 2021 this saw China’s CSSC becoming the biggest military shipbuilder in the world, with arms sales of $11.1 billion, after a merger between two existing companies.’

The combined arms sales of the four South Korean companies in the Top 100 grew by 3.6 percent compared with 2020, reaching $7.2 billion. This was largely due to a 7.6 percent rise in arms sales by Hanwha Aerospace, to $2.6 billion. Hanwha’s arms sales are expected to grow significantly in the coming years, after it signed a major arms deal with Poland in 2022, following the Russian invasion of Ukraine.

Other notable developments

• Six Russian companies are included in the Top 100 for 2021. Their arms sales totaled $17.8 billion—an increase of only 0.4 percent over 2020. There were signs that stagnation was widespread across the Russian arms industry.

• The five Top 100 companies based in the Middle East generated $15.0 billion in arms sales in 2021. This was a 6.5 percent increase compared with 2020, the fastest pace of growth of all regions represented in the Top 100.

• The aggregated arms sales of the four Top 100 companies based in Japan was $9.0 billion, a decline of 1.4 percent compared with 2020.

• This is the first year in which a Taiwanese firm appears in the Top 100. NCSIST (ranked 60th), which specializes in missiles and military electronics, recorded arms sales of $2.0 billion in 2021.

• Private equity companies are becoming more active in the arms industry, particularly in the USA. This could affect the transparency of arms sales data, due to less stringent financial reporting requirements compared with public companies.

SIPRI Arms Industry Database

The SIPRI Arms Industry Database was created in 1989. At that time, it excluded data for companies in countries in Eastern Europe and the Soviet Union. The current version contains data from 2002, including data for companies in Russia. Chinese companies are included in the database from 2015 onwards. The Top 100 listing includes the 100 companies with the largest arms sales during the year covered and for which SIPRI can access sufficient data.

‘Arms sales’ are defined as sales of military goods and services to military customers domestically and abroad. Unless otherwise specified, all changes are expressed in real terms and all figures are given in constant 2021 US dollars. Comparisons between 2020 and 2021 are based on the list of companies ranked in 2021 (i.e., the annual comparison is between the same set of companies). All other year-to-year comparisons are based on the sets of companies listed in the respective year (i.e., the comparison is between different sets of companies). Data for earlier years may be adjusted to reflect new information.

This is the first of three major data launches in the lead-up to the release of SIPRI’s flagship publication in mid-2023, the annual SIPRI Yearbook. Ahead of this, SIPRI will publish its international arms transfers data (details of all international transfers of major arms in 2022) as well as its world military expenditure data (comprehensive information on global, regional and national trends in military spending in 2022).